Latest Manufacturing PMI signals slowest improvement for three months

July 14, 2016 | By MRO Magazine

RBC Canadian Manufacturing PMI

RBC Canadian Manufacturing PMI

RBC Canadian Manufacturing PMI

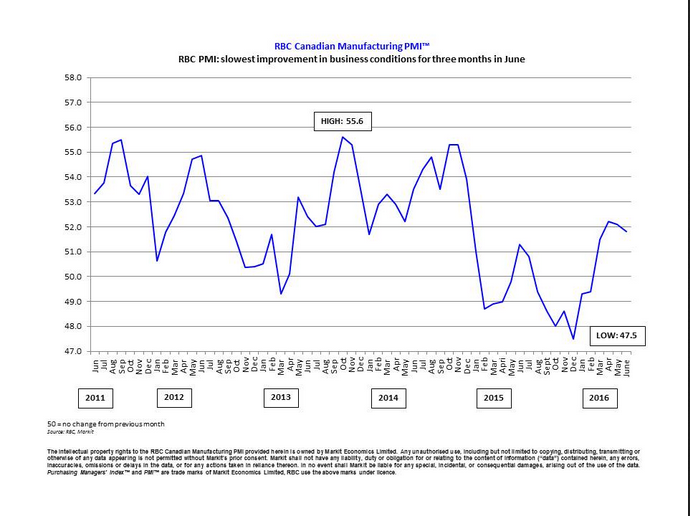

June data suggested that the Canadian manufacturing recovery stepped down a gear at the end of the second quarter, with output, new business and employment growth all easing slightly since May, according to the RBC Canadian Manufacturing Purchasing Managers’ Index (RBC PMI), a comprehensive and early indicator of trends in the Canadian manufacturing sector. Moreover, new export orders were virtually unchanged in June, which contrasted with the solid contribution to growth seen earlier in 2016. At the same time, stocks of finished goods dropped at a survey-record pace in June, with manufacturers noting that subdued client demand and uncertainty about the economic outlook had encouraged tighter inventory management at their plants.

Adjusted for seasonal influences, the RBC Canadian Manufacturing PMI registered 51.8 in June, down from 52.1 in May. (PMI readings above 50.0 signal an improvement in business conditions, while readings below 50.0 signal deterioration.) Although the index posted above the 50.0 no-change value for the fourth month running, the latest reading signalled only a marginal upturn in overall business conditions and the weakest pace of improvement since March.

A slowdown in output growth from May’s 11-month high was on of the key factors weighing on the headline PMI during June. The latest expansion of production volumes was the weakest since March, which manufacturers linked to softer client demand and efforts to reduce finished goods inventories at their plants. Post-production stocks have now fallen in each month since April and the latest reduction was the steepest for over five-and-a-half years.

Canadian manufacturers indicated a marginal upturn in overall new business volumes in June. The latest survey suggested that domestic sales were a key driver of growth, as new export work was broadly unchanged over the month. Higher levels of business underpinned further staff recruitment across the manufacturing sector in June, which extended the current period of net job creation to four months. However, the pace of employment growth eased slightly since May amid reports of heightened uncertainty about the business outlook and a lack of pressure on operating capacity.

Survey respondents pointed to ongoing supply chain pressures in June, with average lead-times from vendors lengthening to the greatest degree since December 2014. This was linked to unusually low stocks at suppliers and a marginal upturn in input buying among manufacturers. Despite a rise in purchasing activity, latest data signalled that pre-production inventories were broadly unchanged over the month, which firms mainly linked to cautious stock policies at their plants.

June data signalled a return to rising factory gate charges among Canadian manufacturers, although the rate of inflation was only marginal. A number of firms noted that subdued underlying demand had acted as a brake on output charge inflation and placed pressure on margins. Moreover, higher steel and fuel prices contributed to a robust rise in average cost burdens in June. The latest increase in overall input prices was the fastest recorded since March.