Canadian manufacturing sector returns to growth in March

April 8, 2016 | By MRO Staff

Canadian manufacturers indicated a positive end to the first quarter, with production and overall new orders returning to growth after a sustained period of decline. Stronger export demand was a key driver behind the rebound in manufacturing conditions, with new work from abroad rising at the joint-fastest pace since November 2014. Survey respondents noted that exchange rate depreciation had encouraged greater focus on export markets in recent months, which helped to boost sales to U.S. clients in particular. Manufacturers nonetheless continued to experience strong input price inflation as suppliers passed on higher imported raw material costs, which contributed to another solid rise in factory gate charges in March.

Canadian manufacturers indicated a positive end to the first quarter, with production and overall new orders returning to growth after a sustained period of decline. Stronger export demand was a key driver behind the rebound in manufacturing conditions, with new work from abroad rising at the joint-fastest pace since November 2014. Survey respondents noted that exchange rate depreciation had encouraged greater focus on export markets in recent months, which helped to boost sales to U.S. clients in particular. Manufacturers nonetheless continued to experience strong input price inflation as suppliers passed on higher imported raw material costs, which contributed to another solid rise in factory gate charges in March.

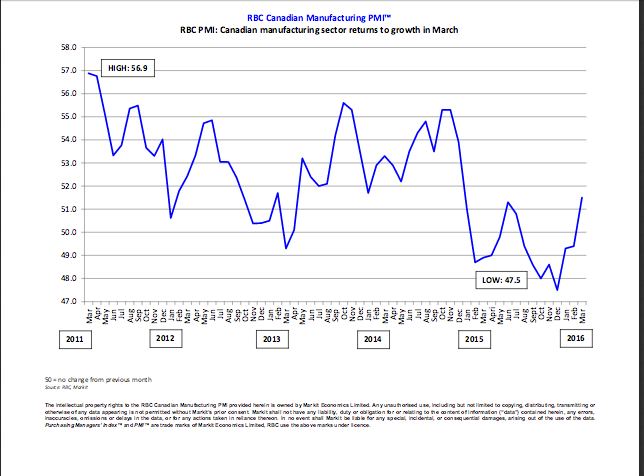

The headline figure derived from the survey is the RBC Canadian Manufacturing Purchasing Managers’ Index (PMI), which is designed to provide timely indications of changes in prevailing business conditions in the Canadian manufacturing sector. PMI readings above 50.0 signal an improvement in business conditions, while readings below 50.0 signal deterioration.

At 51.5 in March, up from 49.4 in February, the seasonally adjusted RBC Canadian Manufacturing PMI posted above the critical 50.0 no-change threshold for the first time in eight months. Moreover, although pointing to only a moderate improvement in business conditions, the index was the highest since December 2014.

Modest rebound in production

The upturn in manufacturing performance was underpinned by a modest rebound in production during March, which ended a seven-month period of falling output volumes. Reports from survey respondents suggested that a combination of stronger demand conditions and the desire to stabilize inventories had acted as a boost to production schedules. Some firms also noted that efforts to improve productivity at their plants had supported output growth in March.

Weak demand in energy sector

Latest data highlighted an increase in overall levels of new work for the first time since August 2015 and, although only moderate, the pace of expansion was the fastest for 15 months. The main reasons cited were greater export sales, new product launches and competitive pricing strategies. Manufacturers also continued to report weak demand from clients in the energy sector. At the same time, new orders from abroad rose for the fifth month running, and the pace of expansion was the joint-fastest since November 2014. Manufacturers continued to report cautious job hiring strategies at their plants. However, the latest survey indicated that overall payroll numbers stabilized in March, thereby ending an eight-month period of falling workforce levels. Meanwhile, a lack of pressure on operating capacity persisted as backlogs of work dropped again across the manufacturing sector.

Renewed production growth and a rebound in new work resulted in greater input buying during March. Although only marginal, the upturn in purchasing activity was the fastest since January 2015. Some firms also noted efforts to boost pre-production inventories amid lower stocks and longer lead-times from suppliers.

On the prices front, latest data pointed to a robust pace of cost inflation. Despite reports of squeezed pricing power, manufacturers passed on a proportion of their higher costs to clients in March, with the rate of charge inflation picking up slightly since February.